This is the annual letter sent out by my friend Richard Poulden. This year – as every year – we wil hold a 10 minute debate at the UKInvestor Show – I am not sure of the subject matter yet but it is always sparky. I am not sure that I agree 100% on China but on Europe we are at one. No debate there. Over to Richard:

“In the absence of the gold standard, there is no way to protect savings from confiscation through inflation” – Alan Greenspan, 1966

“Keep a clear head and always carry a light bulb” – Bob Dylan, 1965

Yesterday morning in Dubai was foggy: thick, gooey, 12-metre visibility stuff. As I drove my daughter to school , I said: “Let’s see how many cars we can find driving without lights”.

“Come on”, she said, “no one could be THAT stupid”

“Oh yes they could”, I said, “I’m going for a starter of three”.

Well we found three cars in the space of a few blocks. As we hit Sheik Zayed Road where the traffic in the fast lane was still doing 120km, she said: “OK, this is crazy, let’s go for 8 or 12”.

“That’s fine”, I said, “but I want to go for the big one: I want to find the European Union…. I want to find a bus..or a large sewage tanker”……and we did.

The gurus at Deutsche Bank published a study1 in July of last year suggesting that the politicians guiding the world economy were behaving exactly like those sewage tankers and buses in the fog. They propose this because their hypothesis is that none of the old economic philosophies actually apply to the current world economy and thus the levers being pulled by the politicians are not actually connected to anything.

Their proposal is quite simple. For most of history, the currency that has circulated in economies has either been itself an item of intrinsic value (gold/silver) or linked to an item of intrinsic value (Bretton Woods and the post WWII exchange rate mechanism). This automatically prevented governments from simply “printing money”. Then, on August 15th 1971, Richard Nixon severed the final link of the US dollar to gold. In so doing he severed the last link of paper currencies to any item of real value. True, international gold convertibility of most major currencies had gone decades before but up until that point the US dollar could still be exchanged for gold at the rate of $35 per ounce.

In 1971 we thus entered a period when, for the first time in history ALL world currencies were “Fiat Currencies”2. The last 41 years have thus been fundamentally different from all preceding economic history, where we have lived in a period where currencies have not been linked to anything other than a government’s statement of what a currency is worth. One of the major problems with this, say Deutsche, is that the economic theories which are now being applied were all developed PRIOR to the Fiat Currency era and thus none of the actions taken in the West are actually relevant to fixing the world economy. Couple this with my hypothesis last year of a tipping point to failure for economies when the state becomes too large a percentage of GDP3 and I suspect we are getting close to an answer as to why the actions of the western politicians since 2008 have had so little effect. If the Swan and Deutsche Bank are right on this then the implications are profound. It means that the European economies (in particular) do not require a bit of stimulus, time to get debt back in line etc. they require a fundamental restructuring like turning round a failed company: I don’t see that happening.

This is a worldwide issue, but unlike Europe, the United States is going to recover. They teeter still on the fiscal cliff and they are gong to run massive deficits under Obama, $1tril plus per year for the rest of his presidency and I know they don’t deserve it, but it is all going to come right.

Never underestimate the underlying strength of the American economy. I have said it before but I’ll say it again… all they have to do is tighten a couple of bolts in the rust belt, get up half an hour earlier and that’s a couple of percentage points on GDP. But now there is something new: cheap energy. Again. Yes, the shale/hard rock oil and gas reserves under the US are going to make them a net energy exporter in a couple of years and mean they can once again ignore world energy prices: US gas is currently about 30% of the European price and may fall.

Obviously this will alter the economics of manufacturing back into America’s favour. Forget cheap labour; in modern manufacturing the cost of energy is almost always the key and this will prove to be America’s salvation. But there are a few other statistics to factor in. They are dramatically counter to what most western press comment, Mitt Romney (RIP) and the entire US Republican Party would have you believe. So…..

Who holds the majority of US Government debt? Is it:

- ) China

- ) Japan

- ) USA

What percentage of products consumed in the US are produced there? Is it:

- ) 25.3%

- ) 58.6%

- ) 88.5%

What is China’s percentage of the above consumption in terms of goods sold in the USA? Is it:

- ) 78.6%

- ) 23.8%

- ) 2.7%

The answer is c) in every case4. China actually only holds around 7.5% of US debt but the vast majority is held by US institutions and individuals. The point here is that this shows you just how disconnected the US economy actually is from the rest of the world. Drawing on the other numbers you can see how a US recovery on the back of cheap energy, regardless of the debt, could happen. Inflation is still going to run and run but that can be good for certain investments like equities and hard assets. Accordingly watch the Dow.

Now let’s take a look at China. Goldman Sachs coined the term “BRICs” as long ago as 2001.5 But the seminal work was “Dreaming with the BRICs” which they published in 2003. In that they predicted that China would overtake the US as the world’s largest economy by 2041. They then revised that to 2027. Now they suggest 2020 and the Economist recently went for 2017. Well I have news for you: if China is not already the largest economy in the world it is certainly the most influential.

Remember the earlier statistics for the percentage of the USA accounted for by China. Remember that China is making massive investments internally. Remember that Internet penetration is still only around 35%: it is about to explode with mobile and the introduction of 4G. Fantastic growth is still there. China will be OK and the rest of the world will benefit from this.

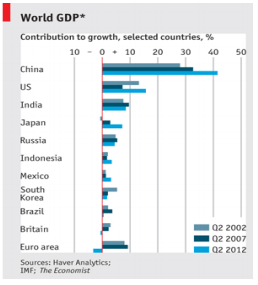

If you look at the graph on the left you can see that China has provided the bulk of world growth since 2002. That is pretty damn influential.

If you look at the graph on the left you can see that China has provided the bulk of world growth since 2002. That is pretty damn influential.

We are seeing the steady introduction of the Chinese currency into world markets. Already ‘offshore’ RMB are freely traded in Hong Kong, Singapore and London. Already many trade transactions are conducted in RMB but I think during 2013 we will see more formal moves to push the RMB onto the world stage.

China is one of the largest holders (and the largest buyer) of gold in the world. Could they..would they..ever push towards gold convertibility for the RMB? I doubt it, as the value of the RMB would soar against all other currencies. But China still has a capacity for infinite surprises.

Conclusions

The same themes of the last few years are still here. Two years ago the Swan predicted that, far from the EU recovering, the rest would drag down the one proper economy in the whole group. At the close of 2012 it seems that is indeed the case as Germany shifts inexorably towards stagnation. There will be no recovery in Europe and there will be increasing social unrest.

Inflation is going to hit big time over the next few years. Look back to my section on fiat currencies. All conventional deposit based savings will thus be destroyed. All pensions managed by a “Fund Manager”, “Insurance Company” or “Independent Financial Advisor” will be useless because they will not place the bets on equities (always just a part of your portfolio) or China and will almost certainly not include enough gold and silver.

I know with both gold and silver flat for 2012 the Swan’s call for gold last year looks weak. However during 2012 money was placed where mouth is and we floated Wishbone Gold in London in July (www.wishbonegoldplc.com ). I remain strong on both gold and silver as hedges on inflation and because of continuing Asian growth, selective commodities in general.

There are also the political and economic wildcards, which can shatter all predictions. As a dweller in the UAE, I hope that the USA does not allow Israel to attack Iran. Recent hope here comes from Obama’s apparent renewed intention to talk.

Bright spots? Continuing growth in Asia and here at home in Dubai the turnaround has come faster and harder than I expected. Driven in part by the “safe haven” view of the UAE but undoubtedly the economy here has turned, new projects are coming on stream and old ones which were mothballed are being restarted.

So to finish on the cars in the fog analogy there’s that old joke that goes: I want to die in my sleep like my grandfather… not screaming in terror like the passengers on his bus. Unfortunately, for those in Europe at least, if you are not screaming already, it is time to start.

All the very best for 2013 and the up coming Year of the Water Snake on 10th

February,

RP

PS: Pictures of “the horror, the horror” as Mr Kurtz once said.

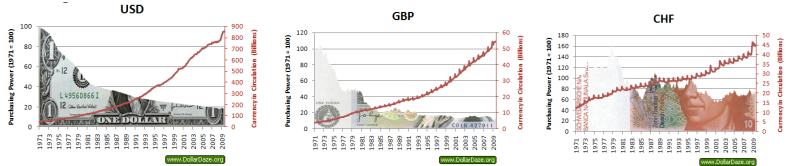

Purchasing power parity on the left scale, currency in circulation on the right. Note performance of Swiss Franc versus the other two.

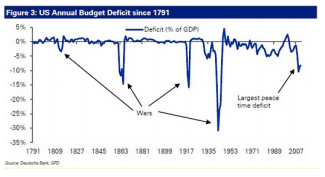

Very neat pic from the Deutsche Bank study. Under Obama this will turn down again..

Very neat pic from the Deutsche Bank study. Under Obama this will turn down again..

Footnotes

1 “Deutsche Bank Annual Long Term Asset Return Study”, Jim Reid, Nick Burns, Stephen Stakhiv

2 Paper money or coins of little or no intrinsic value in themselves and not convertible into gold or silver, but made legal tender by fiat (order) of the government. Source: Financial Times Lexicon.

3 Black Swan News Letter 2012 www.blackswanplc.com

4 Various sources: US Government data, Reserve Bank of San Francisco cited by Kevin Rafferty in South China Morning Post

5 Jim O’Neill then Chief Economist at the Vampire Squid.